Luca Pacioli

Golden rule for nominal accounts

Because these two are getting used at the same time, you will need to understand the place each goes in the ledger. Keep in thoughts that most enterprise accounting software program keeps the chart of accounts flowing the background and also you normally have a look at the primary ledger. Debits increase the balance of dividends, expenses, belongings and losses. Credits enhance the stability of positive aspects, revenue, revenues, liabilities, and shareholder equity. The simplest best way to perceive Debits and Credits is by truly recording them as optimistic and negative numbers immediately on the stability sheet.

Thus, when the customer makes a deposit, the financial institution credit the account (increases the bank’s liability). At the identical time, the financial institution provides the cash to its personal cash holdings account. But the client sometimes doesn’t see this aspect of the transaction. Debits and credit are traditionally distinguished by writing the transfer quantities in separate columns of an account book.

AccountingTools

The left column of the “T” is for Debit (Dr) transactions, whereas the right column is for Credit (Cr) transactions. Each transaction that takes place inside the business will consist of a minimum of one debit to a selected account and a minimum of one credit score to a different particular account. A debit to one account could be balanced by a couple of credit to different accounts, and vice versa. For all transactions, the whole debits have to be equal to the total credits and therefore steadiness. AssetDebits (Dr)Credits (Cr)XThe “X” within the debit column denotes the increasing effect of a transaction on the asset account stability (whole debits much less complete credit), as a result of a debit to an asset account is an increase.

What accountancy means?

Accountancy is the practice of recording, classifying, and reporting on business transactions for a business. It provides feedback to management regarding the financial results and status of an organization. The key accountancy tasks are noted below.

If you obtain $a hundred money, put $a hundred (debit/Positive) next to the Cash account. If you spend $a hundred cash, put -$100 (credit/Negative) subsequent to the money account.

The collection of all these books was referred to as the final ledger. The chart of accounts is the table of contents of the general ledger. Totaling of all debits and credits within the basic ledger on the end of a financial period is known as trial balance.

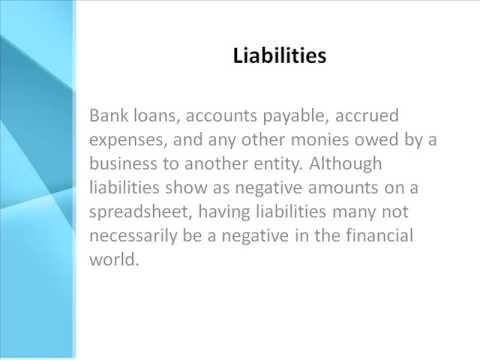

At the end of any financial period (say at the finish of the quarter or the 12 months), the web debit or credit score quantity is referred to as the accounts balance. If the sum of the debit side is larger than the sum of the credit facet, then the account has a “debit balance”. If the sum of the credit score facet is greater, then the account has a “credit score balance”. If debits and credit equal each, then we now have a “zero stability”. Accounts with a web Debit steadiness are generally shown as Assets, while accounts with a internet Credit steadiness are usually shown as Liabilities.

If you bought it as a loan then the -$100 could be recorded subsequent to the Loan Account. If you acquired the $one hundred because you bought something then the $-a hundred can be recorded subsequent to the Retained Earnings Account. If every little thing is seen by way of the steadiness sheet, at a very high stage, then selecting the accounts to make your balance sheet add to zero is the image. The complete accounting equation primarily based on fashionable approach may be very easy to remember if you focus on Assets, Expenses, Costs, Dividends (highlighted in chart).

The asset account above has been added to by a debit worth X, i.e. the stability has elevated by £X or $X. Likewise, within the legal responsibility account beneath, the X within the credit column denotes the rising impact on the liability account balance (complete credit much less whole debits), as a result of a credit score to a legal responsibility account is an increase.

Debits are cash going out of the account; they increase the stability of dividends, expenses, belongings and losses. Credits are cash coming into the account; they improve the stability of features, income, revenues, liabilities, and shareholder fairness. The process of using debits and credits creates a ledger format that resembles the letter “T”. The term “T-account” is accounting jargon for a “ledger account” and is usually used when discussing bookkeeping. The cause that a ledger account is also known as a T-account is because of the way the account is physically drawn on paper (representing a “T”).

- Because these two are getting used on the identical time, it is important to perceive where each goes in the ledger.

- Keep in thoughts that most enterprise accounting software program retains the chart of accounts flowing the background and you often take a look at the principle ledger.

The subsequent step would be to steadiness that transaction with the other sign so that your balance sheet provides to zero. The means of doing these placements are merely a matter of understanding where the money got here from and the place it goes in the specific account types (like Liability and web belongings account). So if $100 Cash got here in and also you Debited/Positive next to the Cash Account, then the following step is to determine where the -$a hundred is classified.

If the entries aren’t balanced, the accountant knows there have to be a mistake somewhere in the general ledger. Before the appearance of computerised accounting, handbook accounting process used a e-book (often known as a ledger) for every T-account.

What is accountancy in simple words?

It is a systematic process of identifying, recording, measuring, classifying, verifying, summarizing, interpreting and communicating financial information. It reveals profit or loss for a given period, and the value and nature of a firm’s assets, liabilities and owners’ equity.

Use ‘accounting’ in a Sentence

Alternately, they can be listed in a single column, indicating debits with the suffix “Dr” or writing them plain, and indicating credit with the suffix “Cr” or a minus sign. Despite the use of a minus signal, debits and credit do not correspond directly to constructive and unfavorable numbers. When the whole of debits in an account exceeds the whole of credit, the account is said to have a net debit balance equal to the difference; when the alternative is true, it has a web credit score steadiness. For a specific account, certainly one of these would be the normal balance kind and might be reported as a constructive quantity, while a negative stability will point out an abnormal situation, as when a checking account is overdrawn. Debit balances are normal for asset and expense accounts, and credit score balances are regular for liability, equity and revenue accounts.

Debits and credits

All these account sorts enhance with debits or left aspect entries. Conversely, a decrease to any of those accounts is a credit score or proper facet entry. On the other hand, will increase in income, liability or fairness accounts are credits or right side entries, and reduces are left side entries or debits. When the shopper pays the invoice, the accountant credit accounts receivables and debits cash. Double-entry accounting is also referred to as balancing the books, as all of the accounting entries are balanced against each other.

The fairness part and retained earnings account, basically reference your revenue or loss. Therefore, that account may be constructive or negative (relying on if you made cash). When you add Assets, Liabilities and Equity together (utilizing optimistic numbers to characterize Debits and adverse numbers to represent Credits) the sum must be Zero. This use of the phrases can be counter-intuitive to folks unfamiliar with bookkeeping concepts, who might at all times think of a credit as a rise and a debit as a lower. A depositor’s checking account is actually a Liability to the bank, because the financial institution legally owes the money to the depositor.

“Day Books” or journals are used to list each single transaction that happened during the day, and the list is totalled on the finish of the day. These daybooks usually are not a part of the double-entry bookkeeping system. The information recorded in these daybooks is then transferred to the overall ledgers. Usually only the sum of the e-book transactions (a batch whole) for the day is entered within the common ledger.

Analysis of GMO food merchandise firms: financial dangers and alternatives in the international agriculture trade

Whenever an accounting transaction is created, no less than two accounts are all the time impacted, with a debit entry being recorded towards one account and a credit entry being recorded against the opposite account. There is not any higher restrict to the number of accounts involved in a transaction – however the minimum is at least two accounts. Thus, using debits and credit in a two-column transaction recording format is essentially the most essential of all controls over accounting accuracy.