Cash-Basis Accounting Definition

REVENUE PROCEDURE ALLOWS ANY COMPANY —sole proprietorship, partnership, S or C company—that meets the sales test to make use of the money method of accounting for tax purposes. If an organization’s average income for the last three years is lower than $1 million, the cash method is allowed but not required. ingle-entry methods, moreover, work well with cash basis accounting, which registers inflows and outflows solely when money flows. Single-entry techniques cannot easily assist the alternative method, accrual accounting—as used by the vast majority of companies worldwide. This model has a operating stability and separate columns for incoming revenues and outgoing bills.

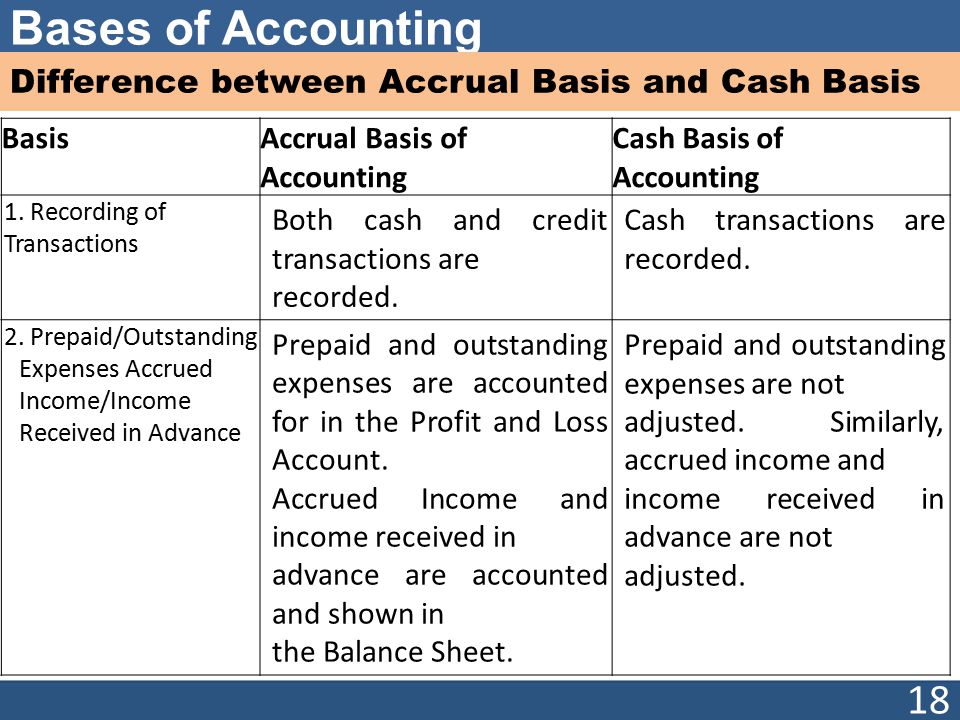

When are bills and revenues counted in accrual accounting?

Income is recorded when it is received, and expenses are reported after they’re truly paid. The cash method is utilized by many sole proprietors and businesses with no inventory.

Accrual basis accounting is the standard strategy to recording transactions for all bigger businesses. This concept differs from the money basis of accounting, under which revenues are recorded when money is acquired, and expenses are recorded when cash is paid.

Cash foundation accounting

Instead, it data transactions only when it either pays out or receives money. The money foundation yields monetary statements which might be noticeably completely different from these created beneath the accrual foundation, since timing delays within the circulate of cash can alter reported results. For instance, a company might avoid recognizing expenses simply by delaying its funds to suppliers.

What is the accrual method of accounting?

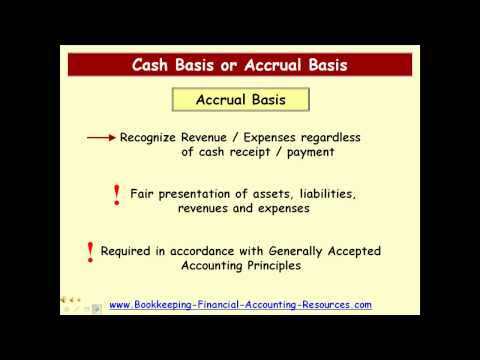

Accrual Accounting. Definition: Accounting method that records revenues and expenses when they are incurred, regardless of when cash is exchanged. The term “accrual” refers to any individual entry recording revenue or expense in the absence of a cash transaction.

Similarly, an accrual foundation firm will document an expense as incurred, whereas a money foundation company would instead wait to pay its supplier before recording the expense. Establishing how you wish to measure your small business’s bills and income is important for monetary reporting and tax functions. However, your small business must select one methodology for income and expense measurement underneath tax legislation and underneath U.S. accounting rules. If a enterprise information its transactions beneath the cash foundation of accounting, then it does not use accruals.

Alternatively, a enterprise might pay payments early so as to acknowledge expenses sooner, thereby lowering its quick-time period revenue tax liability. Accrual accounting requires corporations to document sales at the time by which they occur. Unlike the money foundation method, the timing of actual funds isn’t essential. This could be essential for exhibiting traders the sales revenue the company is generating, the sales trends of the company, and the pro forma estimates for sales expectations.

Accrual Accounting Method

The cash methodology is the most simple in that the books are stored based mostly on the actual circulate of cash in and out of the business. From a tax standpoint, it’s generally advantageous for a brand new enterprise to make use of the money technique of accounting. Cash basis is a serious accounting method by which revenues and bills are only acknowledged when the cost happens. Cash basis accounting is much less accurate than accrual accounting in the quick time period. The primary distinction between accrual and cash basis accounting lies within the timing of when income and bills are acknowledged.

- For monetary reporting functions, U.S accounting standards require companies to operate under an accrual foundation.

- Some small companies that aren’t publicly traded and usually are not required to make many monetary disclosures operate under a cash basis.

- The tax code permits a business to calculate its taxable income using the money or accrual foundation, nevertheless it can’t use both.

From a tax standpoint, it is sometimes advantageous for a new business to make use of the money method of accounting. That means, recording revenue may be put off until the subsequent tax yr, while bills are counted instantly. Accrual accounting is a technique of accounting where revenues and expenses are recorded when they are earned, no matter when the cash is actually acquired or paid. For instance, you’d record revenue when a venture is full, somewhat than whenever you get paid.

Incoming funds are constructive numbers, and outgoing funds are unfavorable numbers (in parentheses). By requiring companies to book income when earned and bills when incurred, GAAP goals to forestall companies from misrepresenting their enterprise activity by manipulating the timing of cash flows. Under cash accounting, a enterprise may avoid recording a loss for, say, the month of June just by holding off on paying its bills till July 1. If September looks like it will be a weak month for gross sales, a company could prop up the numbers by delaying the billing of some prospects in order that their payment does not arrive till after Sept. 1.

With accrual accounting, an organization hoping to control its numbers like this must lie in regards to the timing of revenue and expenses — in other phrases, to commit fraud. Accrual accounting helps a company to maximise its operational skills by spreading out its income recognition and receivables. The increased efficiency advantage is one of the main causes that GAAP requires accrual accounting; the reporting of gross sales is one other.

Incoming revenues are optimistic numbers, and outgoing funds are negative numbers.The record can add further columns, in fact, to point out different categories of revenues or expenses. The only structure required in the register is to include sufficient totally different income and expense categories to meet tax reporting necessities.

This differs from the cash foundation of accounting, beneath which a business recognizes income and bills only when cash is obtained or paid. Two ideas, or rules, that the accrual foundation of accounting uses are the income recognition precept and the matching principle. EXECUTIVE SUMMARY THE IRS RELEASED REVENUE PROCEDURE and income process to give small businesses some much wanted steerage on selecting or altering their accounting methodology for tax functions.

The tax code permits a business to calculate its taxable earnings using the money or accrual basis, however it cannot use each. For financial reporting functions, U.S accounting standards require companies to operate beneath an accrual foundation. Some small businesses that are not publicly traded and are not required to make many monetary disclosures function beneath a cash foundation.

In contrast, if money accounting was used, a transaction wouldn’t be recorded for a while after the merchandise leaves stock. Investors would then be left in the dead of night as to the precise gross sales efficiency and total stock readily available. Managing an organization is a posh course of that includes multiple variables including the capital, revenue, and expenses along with reporting to stakeholders.

Most companies start with a specified amount of capital gained through equity or debt to get their enterprise running and preserve this capital stage for efficient operations. While some small companies could possibly totally manage the business on a cash foundation, it is much more widespread for businesses to stretch out their revenue recognition and receivables over time. A business that makes use of the accrual foundation of accounting recognizes revenue and expenses in the accounting period during which they’re earned or incurred, regardless of when fee occurs.

Accrual Accounting vs. Cash Basis Accounting Example

In basic, accrual accounting offers for a greater sense of a company’s total monetary health than thecash basisaccounting methodology. Let’s assume that I begin an accounting enterprise in December and during December I provided $10,000 of accounting companies. Since I allow purchasers to pay in 30 days, none of the $10,000 of charges that I earned in December were obtained in December. Under the accrual foundation of accounting my enterprise will report the $10,000 of revenues I earned on the December income assertion and will report accounts receivable of $10,000 on the December 31 stability sheet. The cash technique is straightforward in that the business’s books are stored primarily based on the precise circulate of cash in and out of the enterprise.

The “matching precept” is why businesses are required to make use of one technique constantly for each tax and financial reporting purposes. This commonplace states that expenses ought to be acknowledged when the income that creates these liabilities is recognized. Without matching revenues and bills, the overall activity of a business could be significantly misrepresented from interval to interval.