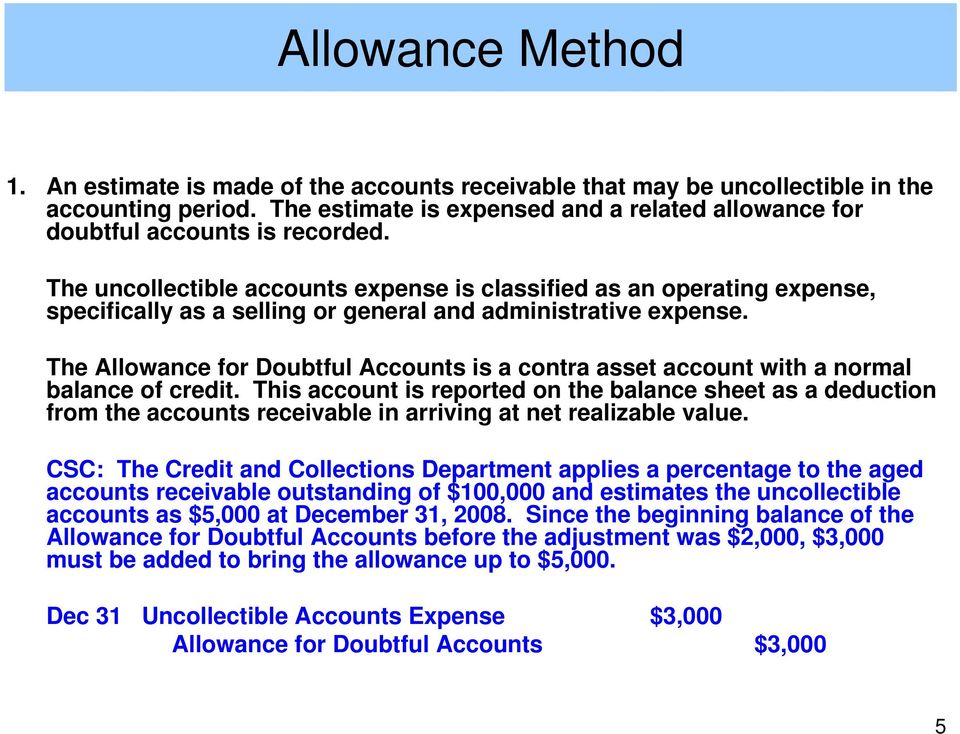

Allowance for Doubtful Accounts

Recording the Allowance for Doubtful Accounts

And when we do that via each of our age classes and add all of it up, we have decided there’s about $15,000 that we expect we might not acquire. So when you put this together with the $900,000 that we’re owed, the amount that we actually count on to collect, that is our possible future financial benefit is $885,000. Based on our definition of asset, that’s the quantity that ought to show up on our steadiness sheet to inform individuals this is the worth we really think that we’ve. We already have our accounts receivable on our T account, and now we have created this contra asset. We name it a contra asset as a result of it offsets the asset off accounts receivable.

Well, we’ll debit our allowance for uncollectible accounts by $2,000. If you think about what we have accomplished right here, we’ve just decreased the asset and its counter asset by exactly the identical amount.

Allowance For Doubtful Accounts

Now, we’re just going to do the same process we did earlier than, we’re going to go ahead and age the accounts. We have new info now, although, we would know something particularly about some of the clients. The macro surroundings might have changed, as a result of it is our second year in business, we may have higher sense of what’s going to be normal in our accounts. You can see right here that we upped our estimate to 1% of our present not being collected. And we’ve changed some of our other estimates as well, in particular, our over ninety days quantity.

Allowance for doubtful accounts calculation

We can add in all the exercise from this era, our $10,000,000 of gross sales, our $9,900,000 of collections, which gets us to our ending stability of $1,000,000. Now the query turns into, how huge of an allowance for uncollectible accounts do we have to have associated to that $1,000,000? And then what is the mirrored bad debit expense that we will should incur in order to get us to that balance?

The query turns into, what concerning the probable future financial benefit? At the top of 2015 they have a $900,000 balance of their accounts receivable, that is individuals owe them $900,000 that they have not paid them but.

They’ve gone out of business and our attorneys inform us there’s really no approach to collect that amount. Well, now we’d have a look at our accounts receivable and say, despite the fact that legally we have been owed $1 million, we all know we’re not going to gather $2,000 of that. So we’ll have to scale back that asset with the $2,000 credit, how will we get that entry to steadiness?

Welcome, within the last couple of videos we have mentioned income recognition and the way to handle that from an accountant standpoint. In this video, we’re going to talk about a associated item, which is accounts receivable. You usually receive accounts receivable in return for whatever it is you have given as much as create revenue. Now, before we get into the details of accounts receivable, it’s in all probability worthwhile to review our definition of an asset from quite a couple of movies ago.

At this level, we have all of our financial statements right primarily based on these expectations. And there’s only one concern still hanging out there, which is what can we do as soon as we determine really who’s not going to pay us? Remember, that $21,000 was primarily based on expectations the place we thought in regards to the basic market, in addition to some particular data we had. Let’s think about that, firstly of the subsequent period, January 5th, say, of 2017, we find out that Jones, Inc just isn’t going to pay us $2,000 that they owe us.

- Welcome, within the last couple of movies we have mentioned income recognition and how to deal with that from an accountant standpoint.

- In this video, we’ll talk about a related item, which is accounts receivable.

There was a past transaction, there was a sale and it is underneath my management. I actually have the legal proper to pursue fee to that in case somebody tries to not pay me.

So this is really taken this steadiness sheet type of perspective of let’s get that probable future economic profit that meets the definition of an asset right. And then the revenue assertion is just no matter has to occur to be able to get our stability sheet correct. Well, we might report $979,000 of net accounts receivable, that’s the expected collections, not what’s really as a result of us of the million, however we are expect we will gather in this state of affairs. Our income assertion’s going to reflect that $6,000 of extra loss this era due to dangerous debt expense.

We got our balance sheet proper, we discovered it’s about $885,000 of possible future economic benefit. And then we reflected on our earnings statement an quantity that was wanted in order to get that stability sheet to the right amount. This could be a little clearer to you if we go ahead and have a look at the next yr for this firm. They’ve already collected on $9,900,000 of these credit gross sales and so there’s $1,000,000 left of their stability.

And the associated unhealthy debt expense because of the fact that they are not going to get this value. Well, typically the best way to go about this may be to begin with something we name the growing older of the accounts.

When we add all of this up, we’ve now increased our allowance for uncertain accounts to $21,000. So once we put that amount as much as $21,000, we all know that we’re going to should credit score our contra asset allowance for uncollectible accounts for $6,000. Well, identical to final time, our income assertion displays the fact that we have now misplaced $6,000 more worth in expectation. Again, discover that we obtained our stability sheet proper, and our revenue assertion was just no matter it wanted to be.

When is revenue recognized beneath accrual accounting?

That’s the place you’re taking all the accounts and also you break them down into categories based on how far overdue are they. You can see in this instance, a big portion of our accounts are literally current, folks aren’t supposed to have paid us but. You’d undergo all of these accounts, and also you’d have a look at not solely how far past due they are, however what do I know about them? For instance, maybe that 90 day handed due quantity is a disputed amount the place the consumer’s saying, you did not actually send me what I requested for, or the objects you sent me weren’t of high sufficient high quality.

And you could recall that there’s three criteria to having an asset. The first is a probable future economic profit, underneath my management and it comes from a past transaction. When we look at the account’s receivable, we meet the ultimate two standards pretty easily.

We’re going to call this contra asset our allowance for uncollectible accounts. That’s that $15,000 that represents our estimate that of the $900,000 there’s about $15,000 we’re not going to be able to collect in the long run. Now, once we put together our steadiness sheet to supply to outsiders, what we’re going to present is a internet accounts receivable of $885,000. Of course, whenever you have a look at that, you ask yourself, nicely, the place did that $15,000 go then that I now say I’m not going to collect?

Well, we will show that on the income assertion as one thing we name unhealthy debt expense. That reflects the price of having done enterprise throughout this era and not being able to collect on some of the things that our customers owe us.

Maybe in some conditions, we’ve some sense that, just generally, the geographic space of the country that the consumer’s doing enterprise in isn’t doing nice. We’ll attempt to combine these more basic phrases together with our specific knowledge to provide you with some estimate of quantities we’re not going to collect. Those will lead to a proportion that we consider we won’t collect. We don’t know exactly which of these people will not pay us, but our estimate is that some portion of them won’t.